5 Massive Real Estate Trends Created by the Pandemic

Coronavirus has had a huge impact on a number of demographic and home buying and selling trends. Here are 5 of the most noteworthy shifts.

The coronavirus pandemic upended daily American life in countless unpredictable ways. Real estate was no exception. Some of the ways in which the pandemic affected housing reshape how we think about homeownership and hint at larger economic shifts down the line.

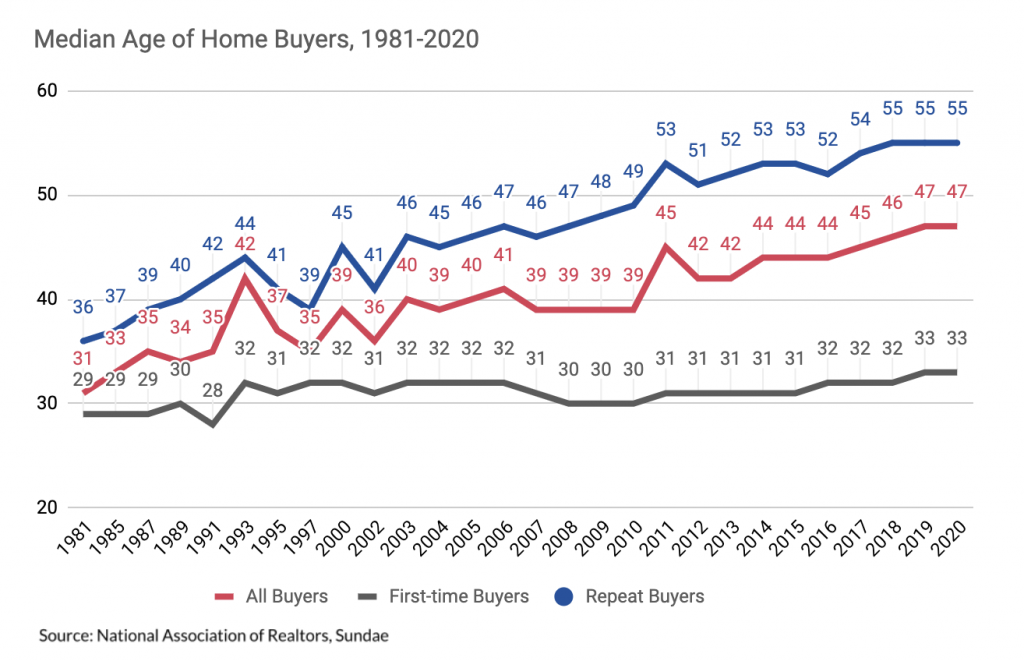

First-time buyer demographics prior to 2020

The median age of first-time homebuyers was around 33 before the pandemic started. This is the oldest age recorded since 1981 when the median age of first-time homebuyers was 29.

As homeownership is commonly considered a gateway to wealth creation and a key piece of the American dream, an older average first-time buyer age could reflect a lack of economic opportunity for young people.

Over the past few decades, there were several factors behind the extra four years it takes on average to buy a first home. Contributing factors include:

- A skyrocketing increase in college tuition

- Delay in household formations (i.e. having children later)

- Rapid home appreciation causing lack of affordability

Other key demographic trends predating the pandemic

The median age of repeat buyers increased even more rapidly between 1981 and 2020, going from 36 to 55. As with first-time home buyers, multiple interesting factors drove this trend. For example, some studies claim that baby boomers prefer to age in place, identifying 3.6 million unoccupied rooms owned by baby boomers, thus contributing to the housing shortage.

But it’s not that simple.

Since 1980, wage growth hasn’t kept up with inflation for over 50% of American workers. Meanwhile, the dot.com bust and the Great Recession dropped S&P levels 43% and 48%, respectively, which also reduced home equity at a similar level. This essentially trapped boomers because they owed more on their homes than they could get for them, while at the same time suffering hits to their overall wealth.

The Great Recession also created an opportunity for older Gen Xers and boomers with cash to purchase investment properties. As home prices dipped following the bubble bust, Americans seized their chance to buy properties for passive income, and with more distressed properties for fix and flip opportunities, real estate became a more popular way for people above median home buying age to create wealth, thus contributing to the increased repeat buyer age.

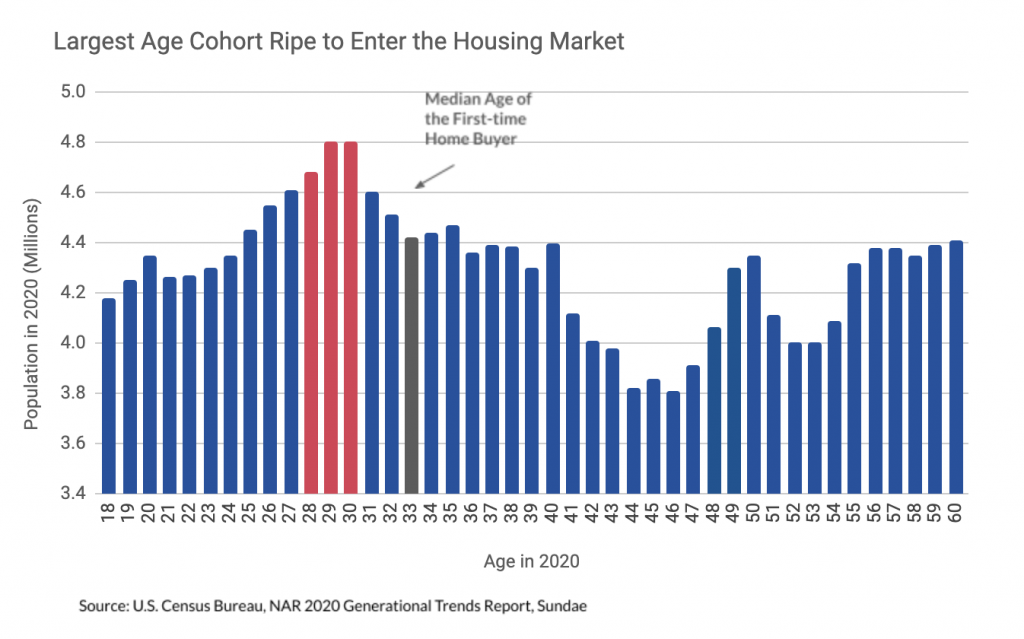

The biggest jolt in demand is yet to come

The largest age bracket among millennials, which adds up to nearly 10 million people, has been turning 30 over the last two years. This is the milestone age of starting a family and buying a home.

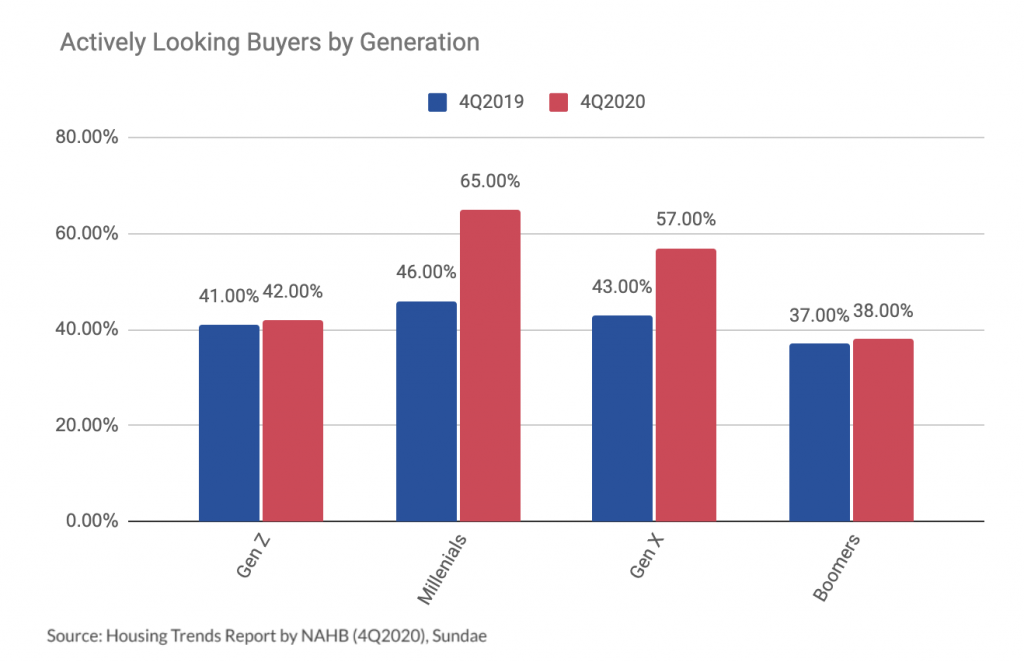

Their home-buying appetites are already starting to show.

According to the NAHB Trends Report, between the fourth quarter of 2019 and that of 2020, the number of millennials and gen Xers actively searching for a home increased dramatically, from 46% to 65% and 43% to 57%, respectively. The relative numbers of gen Zers and boomers remained essentially flat, with 42% and 32% looking for a home, respectively.

With this demographic backdrop, and the continuing economic and social fallout from the coronavirus, what are we likely to see over the remainder of 2021 and beyond?

Trend #1: Median age of first-time homebuyers will decline

Millennials’ desire to own a home has been long debated. A number of long-term trends put millennial homeownership on the backburner:

- Marrying and having children at an older age than generations before

- Massive increases in student debt that hinder the ability to save up for a downpayment

- Stagnant income growth compared to housing appreciation

Interestingly, the COVID-19 pandemic created an attracted new opportunity for this demographic cohort. Several things came together: immediate demand for more space with the need to work from home, record low-interest rates that translate to lower monthly mortgage payments, and the last piece of the puzzle, increased savings.

While staying home, there is no need to buy new clothes or daily Starbucks. There is no going out after work or on weekends, and a lot less travel, for work or pleasure. In fact, the virus even put a pause on paying off college debt, since it became a COVID-19 Relief option.

The bottom line is that more people will have the ability and interest to buy a house, sooner than they were before.

Trend #2: Median age of repeat home buyers will decline

The median age of repeat home buyers is likely to decline immediately post-pandemic, but will revert to the pre-pandemic increasing trend quickly.

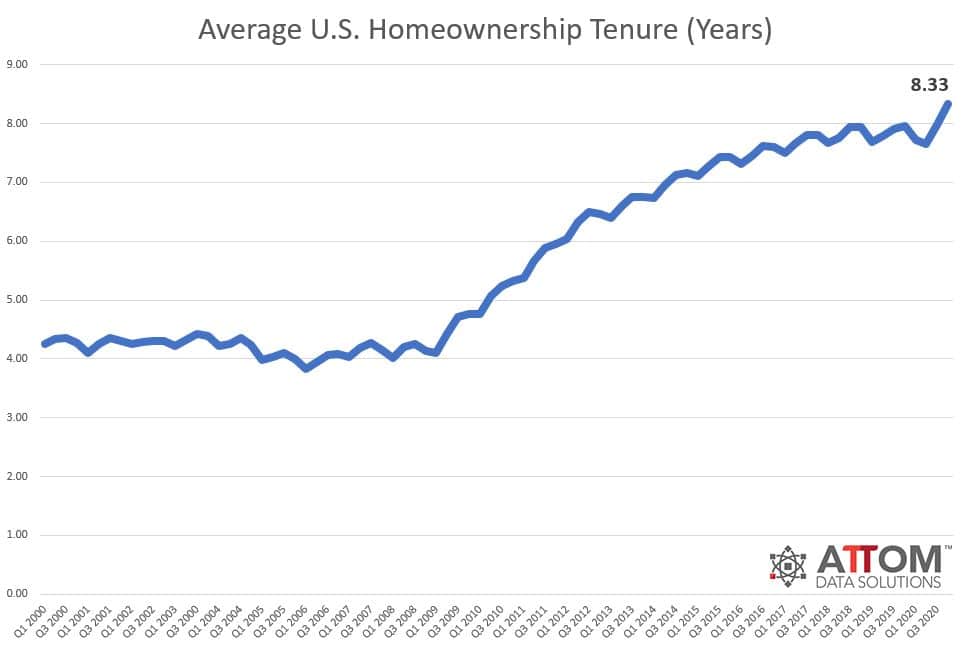

The average tenure of homeownership continued to increase and was over 8 years at the end of 2020, up from 4 years in 2007, before the Great Recession. Assuming the median age of the typical “move up,” or second-time home buyer is roughly 40 years old (given the simple math of 33 + 8), a median repeat buyer age around 55 means that a lot more people in their 50s, 60s and 70s are acquiring third, fourth, or even fifth properties.

{kind=link}

One of the factors behind the dramatic age increase in repeat buyers since 1981 is the growing popularity of real estate as an investment. During the Great Recession, mom and pop investors who had cash and solid credit were able to build their rental income portfolios by capitalizing on depressed home prices and strong rental demand from distressed homeowners.

Another factor is the baby boomer generation born between 1940 and 1964 has been downsizing. According to the latest Census data, many baby boomers will be single in retirement. Almost a third of men and over half of women are unmarried at 65 or older.

With the onset of the pandemic, city dwellers who could work remotely and whose kids started going to school virtually began looking for bigger houses and open spaces in rural areas. With interest rates at historic lows, amid the pandemic, it became a strangely perfect time to buy a dream vacation home away from major Metropolitan Areas.

The annual rise in second-home mortgage applications is more than double the increase in mortgage applications for primary homes, with demand driven primarily by families with kids. Aside from vacation homes, working, learning, dining, working out, and self-entertaining at home created the need for more space and put a larger value on the fourth bedroom or larger back yard.

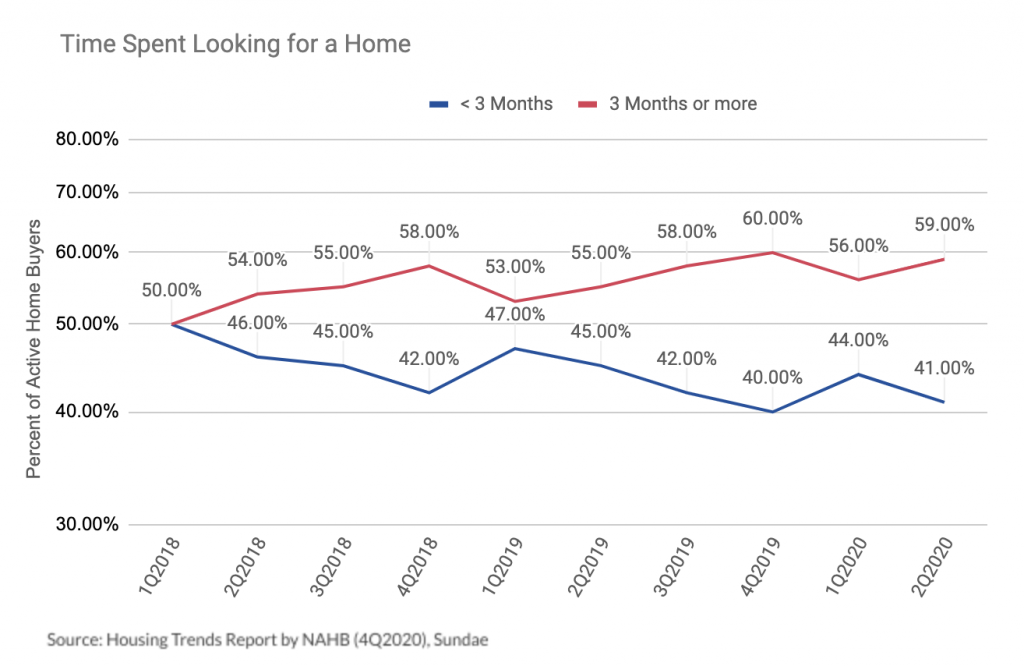

Trend #3: Length of the home search process increased and will keep increasing

Lack of supply set the trend for buyers to view fewer homes while the home purchase process itself is increasing.

Tight inventory results in fewer homes on the market, and buyers must search longer for the right home. With fewer homes available, there are fewer homes that fit the buyers’ requirements coming on the market. On top of that, in the Housing Trends Survey the number one reason 40% of home searchers cited, is being outbid by other offers as opposed to not being able to find an affordably priced home, which is a big difference from 19% of home searchers a year ago.

Trend #4: Fewer sacrifices will be made to purchase a home

Financial experts recommend having three to six months’ worth of expenses saved up in an emergency account. But at the end of 2019, according to GoBankingRates survey, 69% of Americans have less than $1,000 in savings. The personal savings rate, or amount people are saving as a percentage of their disposable income, soared to 33% in April of 2020. That was the highest savings rate recorded since BEA started tracking it in 1959. People realized the importance of having emergency funds and at the same time, stimulus payments and tax refunds have been distributed to help build up a reserve.

Per Generational Trend Report from NAR, in order to save for a downpayment, home buyers had to cut spending on non-essential items, entertainment, clothes, vacations, get a second job or sell a car. But with severe limitations on how money can be spent, savings built up on their own.

| All Buyers | 22 to 29 | 30 to 39 | 40 to 54 | 55 to 64 | 65 to 73 | 74 to 94 | |

|---|---|---|---|---|---|---|---|

| Cut spending on luxury items or non-essential items | 28% | 46% | 37% | 28% | 19% | 11% | 9% |

| Cut spending on entertainment | 21% | 35% | 29% | 23% | 12% | 8% | 3% |

| Cut spending on clothes | 16% | 29% | 23% | 15% | 10% | 7% | 2% |

| Canceled vacation plans | 9% | 9% | 11% | 13% | 7% | 6% | 2% |

| Paid minimum payments on bills | 9% | 17% | 12% | 10% | 6% | 2% | 1% |

| Earned extra income through a second job | 6% | 11% | 8% | 6% | 3% | 2% | * |

| Sold a vehicle or decided not to purchase a vehicle | 5% | 7% | 6% | 7% | 4% | 1% | 2% |

| Other | 5% | 4% | 3% | 7% | 5% | 5% | 6% |

| Did not need to make any sacrifices | 59% | 41% | 50% | 55% | 69% | 78% | 82% |

Source: Generational Trends. Report. National Association of REALTORS®

Trend #5: Fewer repeat buyers will compromise on the top four reasons

With so few homes for sale, the additional risks of holding an open house to sell their own, and having crowds doing walkthroughs, move up buyers are likely to stay put unless a property that meets most of their needs is identified and won in a bidding war.

| All Buyers | 22 to 29 | 30 to 39 | 40 to 54 | 55 to 64 | 65 to 73 | 74 to 94 | |

|---|---|---|---|---|---|---|---|

| Price of home | 25% | 24% | 29% | 25% | 21% | 23% | 19% |

| Condition of home | 23% | 25% | 23% | 23% | 23% | 18% | 20% |

| Size of home | 19% | 17% | 22% | 20% | 20% | 13% | 17% |

| Style of home | 16% | 21% | 18% | 17% | 14% | 11% | 13% |

| Lot size | 15% | 17% | 18% | 14% | 13% | 11% | 11% |

| Distance from job | 13% | 20% | 20% | 15% | 9% | 3% | 2% |

| Distance from friends or family | 7% | 10% | 9% | 6% | 5% | 7% | 8% |

| Quality of the neighborhood | 7% | 8% | 8% | 6% | 5% | 5% | 7% |

| Quality of the schools | 3% | 7% | 6% | 2% | 1% | 1% | * |

| Distance from school | 2% | 1% | 3% | 3% | 1% | * | * |

| None -Made no compromises | 29% | 18% | 21% | 29% | 34% | 42% | 51% |

| Other compromises not listed | 8% | 9% | 6% | 8% | 10% | 10% | 7% |

Source: Generational Trends. Report. National Association of REALTORS®

Not only have public health concerns necessitated virtual tours, but home buyers are getting savvier with online tools. Even before the pandemic, 93% of homebuyers used the internet as a resource in their home search, according to the NAR.

Sellers are having to keep up with the trends, too.

Further Reading: Real Estate Shifts to Accommodate Customers in a Virtual Age

What will be the big theme for 2021?

To start, a massive fear of missing out.

The headlines of every major media outlet are screaming about continuous home price appreciation. The thought of home prices reaching the point of being out of reach while interest rates have nowhere to go but up will be the end of the last opportunity to buy that first, or second, or even an investment property.

With a tight, low-inventory market dipping under 2 months of supply, the strongest contract activity in a decade, and historically low-interest rates, buyers’ fear is well-founded and likely to only get worse.

But don’t take our word for it.

Ready to Get Started?

Sell as-is. Pay zero fees to Sundae. Move on your time. No repairs, cleanings, or showings.

Polina is Sundae's Sr. Director of Research and Lead Economist. She has more than 15 years of valuation experience across commercial and residential real estate. Her background includes stints with Cushman & Wakefield, Hanley Wood, and Standard & Poor’s. Polina graduated with a double major in Economics and International Relations from the University of California at Davis and has been a CAIA Charter Holder since 2010.